January Market Update

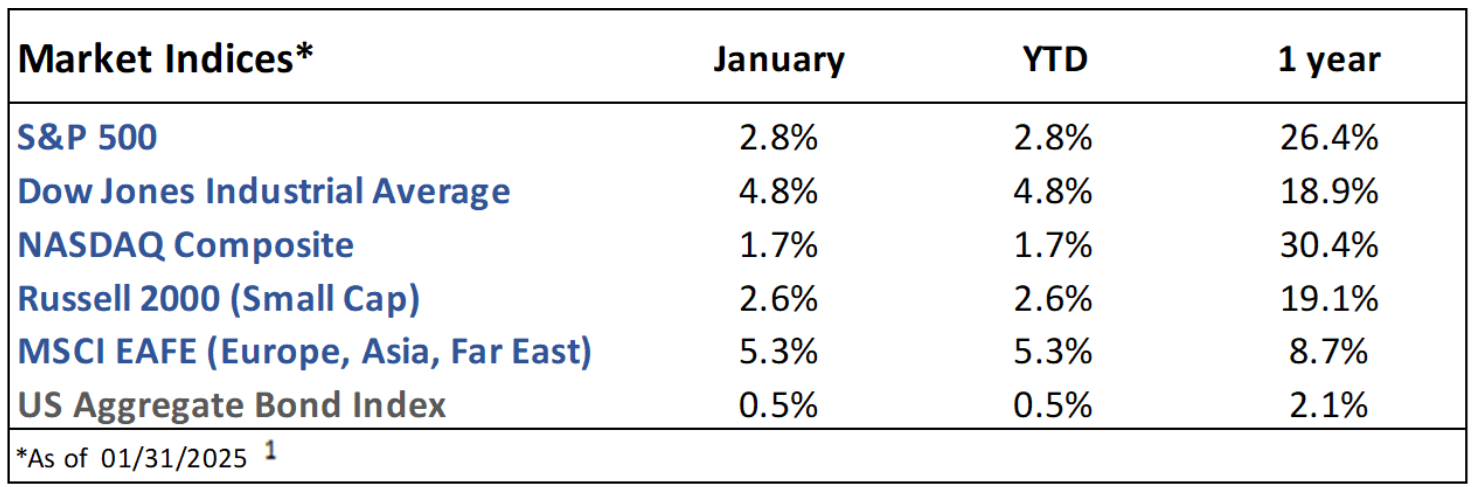

Market Indices Performance

January Recap

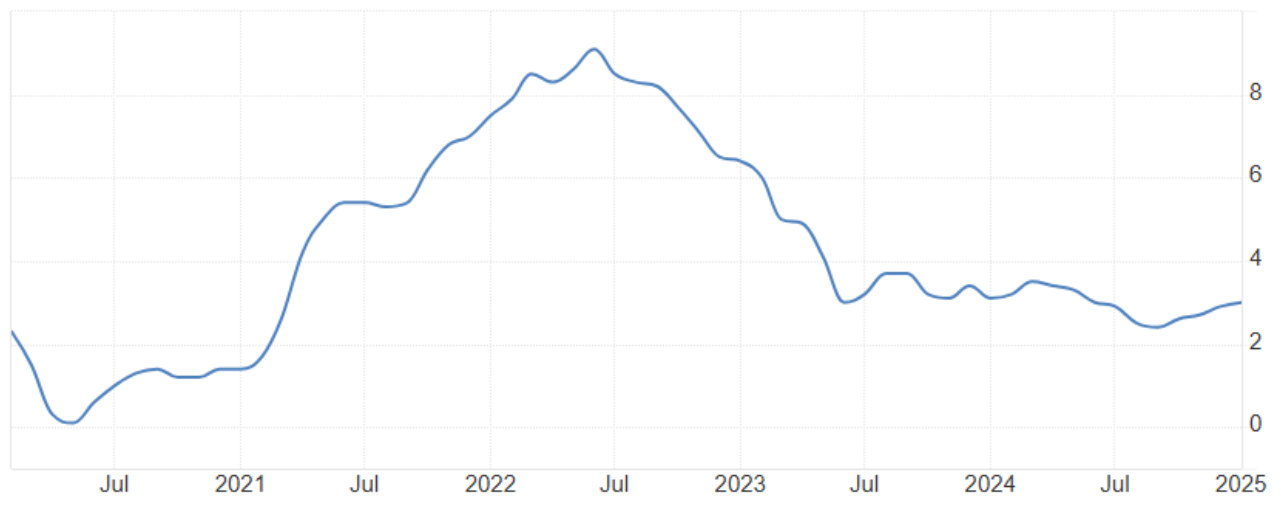

The S&P 500 rose 2.8% in January; International stocks outperformed but have significantly underperformed over the past couple of years.(1) The 10yr Treasury finished January lower after spiking in the middle of the month as investors anticipated elevated growth and inflation from tariffs under the Trump administration. The Federal Reserve held interest rates steady at a level of 4.25-4.50%. Inflation, measured by the Consumer Price Index (CPI), rose 3.0% from last year, marking the 47th straight month above the Federal Reserve’s 2% target (figure 1).(2) The economy added 143k jobs, lower than the 160k expected, but December’s report was revised higher by 50k jobs. The unemployment rate fell slightly to 4.0% and has been in the 4.0%-4.3% range for nine straight months.(3) Job openings fell to 7.6m, but the ratio of jobs available to unemployed people remains healthily above 1.(4) All this points to a continually strong labor market.

The Present

Q4 earnings season is now underway, with expectations for 11.7% growth.(5) Much of the focus will once again be on the Magnificent 7 stocks(6) and their AI spending. President Trump has issued 25% tariffs on steel and aluminum beginning in March, additional 10% tariffs on China, reciprocal tariffs (matches other countries tariffs on our goods), and 25% tariffs on Canada and Mexico that are on hold until early March.(7) Should these tariffs last, Americans should expect an uptick in inflation. The 10yr Treasury has risen from 3.6% in September to ~4.6% today despite 1% worth of cuts to the federal funds rate during that time (see figure 2).(8) This is a good reminder that the very short-term federal funds rate being changed will not necessarily result in an equal change in longer-term rates, such as auto loans or mortgages. Mortgage rates have bounced between 6%-8% since the beginning of 2023, and now sit just below 7%.(9)

The Future

Analysts predict earnings growth of 15% for 2025.(5) The Federal Reserve and Wall Street predict 1-2 interest rate cuts this year, but that will all depend on inflation and the labor market.(10,11) February has historically been a rough month for the stock market.(12) There remains widespread uncertainty around President Trump’s policies on tariffs, lowering taxes, cracking down on immigration, and increasing oil production in the US.(13) These policies have the potential to negatively and positively affect the economy and the markets, but we and most of Wall Street remain cautiously optimistic overall on the Trump administration.

1. https://ycharts.com/indices/%5ESPXTR, https://ycharts.com/indices/%5EDJITR, https://ycharts.com/indices/%5ENACTR, https://ycharts.com/indices/%5ERUTTR, https://ycharts.com/indices/%5EMSEAFETR, https://ycharts.com/indices/%5EBBUSATR – Index Performance

2. https://www.investing.com/economic-calendar/cpi-733 - CPI

3. https://www.investing.com/economic-calendar/nonfarm-payrolls-227 - Jobs reports

4. https://fred.stlouisfed.org/graph/?g=12kNG - Job openings

5. https://advantage.factset.com/hubfs/Website/Resources%20Section/Research%20Desk/Earnings%20Insight/EarningsInsight_011025A.pdf - Earnings expectations

6. The Magnificent 7 stocks are Apple, Microsoft, Google parent Alphabet, Amazon.com, Nvidia, Meta Platforms, and Tesla

7. https://taxfoundation.org/research/all/federal/trump-tariffs-trade-war/ - Tariffs

8. https://www.cnbc.com/bonds/ - Treasury yields

9. https://fred.stlouisfed.org/series/MORTGAGE30US - Mortgage Rates

10. https://www.cmegroup.com/markets/interest-rates/cme-fedwatch-tool.html – Investor rate expectations

11. https://finance.yahoo.com/news/fed-cuts-rates-by-quarter-point-scales-back-cuts-for-2025-125715874.html - Fed Outlook

12. https://www.nasdaq.com/articles/heres-the-average-stock-market-return-in-every-month-of-the-year – Monthly market history

13. https://taxfoundation.org/research/all/federal/donald-trump-tax-plan-2024/ - Trump presidency likely outcomes

The Gasaway Team

7110 Stadium Drive

Kalamazoo, MI 49009

(269) 324-0080

FAX (269) 324-3834

The views expressed are those of the author as of the date noted, are subject to change based on market and other various conditions. This presentation is not an offer or a solicitation to buy or sell securities. The material discussed is meant to provide general education information only and it is not to be construed as specific investment, tax or legal advice and does not give investment recommendations.

Certain risks exist with any type of investment and should be considered carefully before making any investment decisions. Keep in mind that current and historical facts may not be indicative of future results.

Additional information, including management fees and expenses, is provided on our Form ADV Part 2 available upon request or at the SEC’s Investment Adviser Public Disclosure website, https://adviserinfo.sec.gov/firm/summary/123807.

This material was created for educational and informational purposes only and is not intended as ERISA, tax, legal, or investment advice. If you are seeking investment advice specific to your needs, such advice services must be obtained on your own separate from this educational material. ©401(k) Marketing, LLC. All rights reserved. Proprietary and confidential. Do not copy or distribute outside original intent.