October Market Update

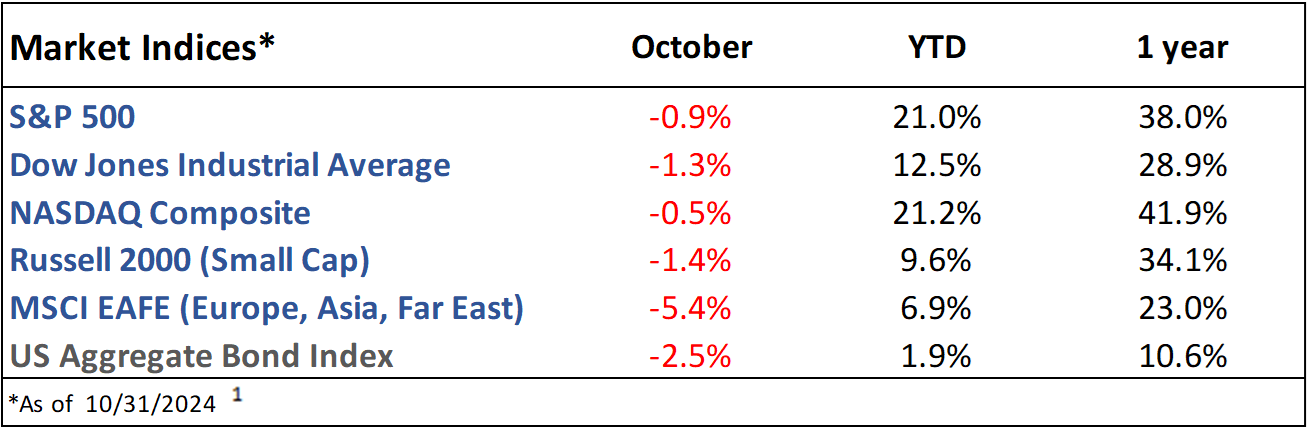

Market Indices Performance

October Recap

Stocks were down across the board in October, and rising yields led to bonds falling as well. Inflation, measured by the Consumer Price Index (CPI), rose 2.6% from last year, much lower than the 9.1% peak in 2022 but up from 2.4% in September and marking the 44th straight month above the Federal Reserve’s 2% target.(2) The economy only added 12k jobs, the lowest amount since January 2021, mostly thanks to the hurricanes and a strike at Boeing. The unemployment rate remained at 4.1%.(3) Job openings fell to 7.4m, but the ratio of jobs available to unemployed people remains slightly above 1 (figure 1).(4)

Figure 1. Job openings to unemployed ratio (4)

The Present

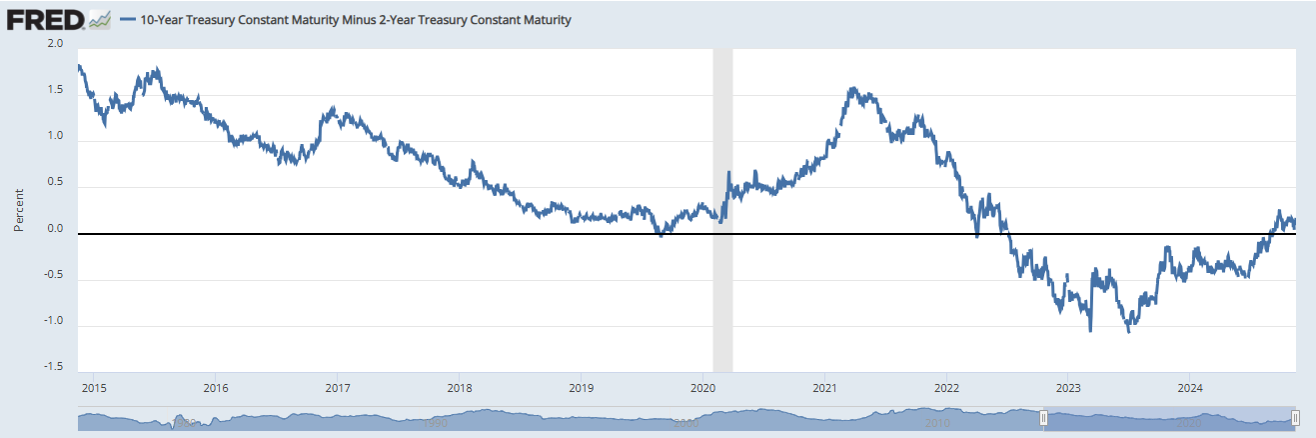

As you likely know, Donald Trump won the presidential election and will be inaugurated on January 20, 2025. Q3 earnings season is around 90% complete; earnings growth has been ~5% vs ~4% expected.(5) As expected, the Federal Reserve cut interest rates by 0.25% to a new level of 4.50%-4.75% on November 7; however, they were a little less optimistic about inflation’s path to 2% than at their last meeting. Bond yields continue to respond to positive economic data and outlooks; the 10yr Treasury has risen from 3.6% to 4.4% since the Fed CUT interest rates by 0.50% in September (and now another 0.25% in November). The 2yr Treasury has risen from 3.6% to 4.2%.(6) After over 2 years of the 2yr/10yr yield curve being inverted (2yr Treasury yields being higher than 10yr Treasury yields), the curve has been ‘normal’ (upward-sloping) since early September (figure 2).(7) Mortgage rates have crossed back above 6.5%.(8)

Figure 2. 2yr/10yr Yield Spread (7)

The Future

Analysts expect earnings growth of 15% in 2025 after 9% in 2024.(9) The market is predicting another 0.25% interest rate cut in December, which would be in line with the latest Fed predictions.(10,11) November has historically been a slightly above-average month for the market.(12) As for the Trump presidency, he is planning to usher in increased tariffs (likely triggering at least a short-term rise in prices), lower taxes (by extending the Tax Cuts and Jobs Act and introducing additional tax eliminations), less immigration (likely reducing the labor force), less regulation (likely spurring economic growth), and more domestic oil production (likely easing inflationary pressures across the board).(13)

2. https://www.investing.com/economic-calendar/cpi-733 - CPI

3. https://www.investing.com/economic-calendar/nonfarm-payrolls-227 - Jobs reports

4. https://fred.stlouisfed.org/graph/?g=12kNG - Job openings

5. https://www.reuters.com/markets/asia/china-markets-reopen-with-roar-after-week-long-break-2024-10-08/ - Earnings

6. https://www.cnbc.com/quotes/US10Y/ - Treasury Yields

7. https://fred.stlouisfed.org/series/T10Y2Y - Yield Curve

8. https://fred.stlouisfed.org/series/MORTGAGE30US - Mortgage Rates

9. https://advantage.factset.com/hubfs/Website/Resources%20Section/Research%20Desk/Earnings%20Insight/EarningsInsight_100424.pdf - Earnings expectations

10. https://www.cmegroup.com/markets/interest-rates/cme-fedwatch-tool.html – Investor rate expectations

11. https://finance.yahoo.com/news/fed-dot-plot-suggests-central-bank-will-slash-interest-rates-two-more-times-in-2024-after-mega-50-basis-point-cut-182511834.html - Fed Outlook

12. https://www.nasdaq.com/articles/heres-the-average-stock-market-return-in-every-month-of-the-year – Monthly market history

13. https://taxfoundation.org/research/all/federal/donald-trump-tax-plan-2024/ - Trump presidency likely outcomes

The Gasaway Team

7110 Stadium Drive

Kalamazoo, MI 49009

(269) 324-0080

FAX (269) 324-3834

The views expressed are those of the author as of the date noted, are subject to change based on market and other various conditions. This presentation is not an offer or a solicitation to buy or sell securities. The material discussed is meant to provide general education information only and it is not to be construed as specific investment, tax or legal advice and does not give investment recommendations.

Certain risks exist with any type of investment and should be considered carefully before making any investment decisions. Keep in mind that current and historical facts may not be indicative of future results.

Additional information, including management fees and expenses, is provided on our Form ADV Part 2 available upon request or at the SEC’s Investment Adviser Public Disclosure website, https://adviserinfo.sec.gov/firm/summary/123807.